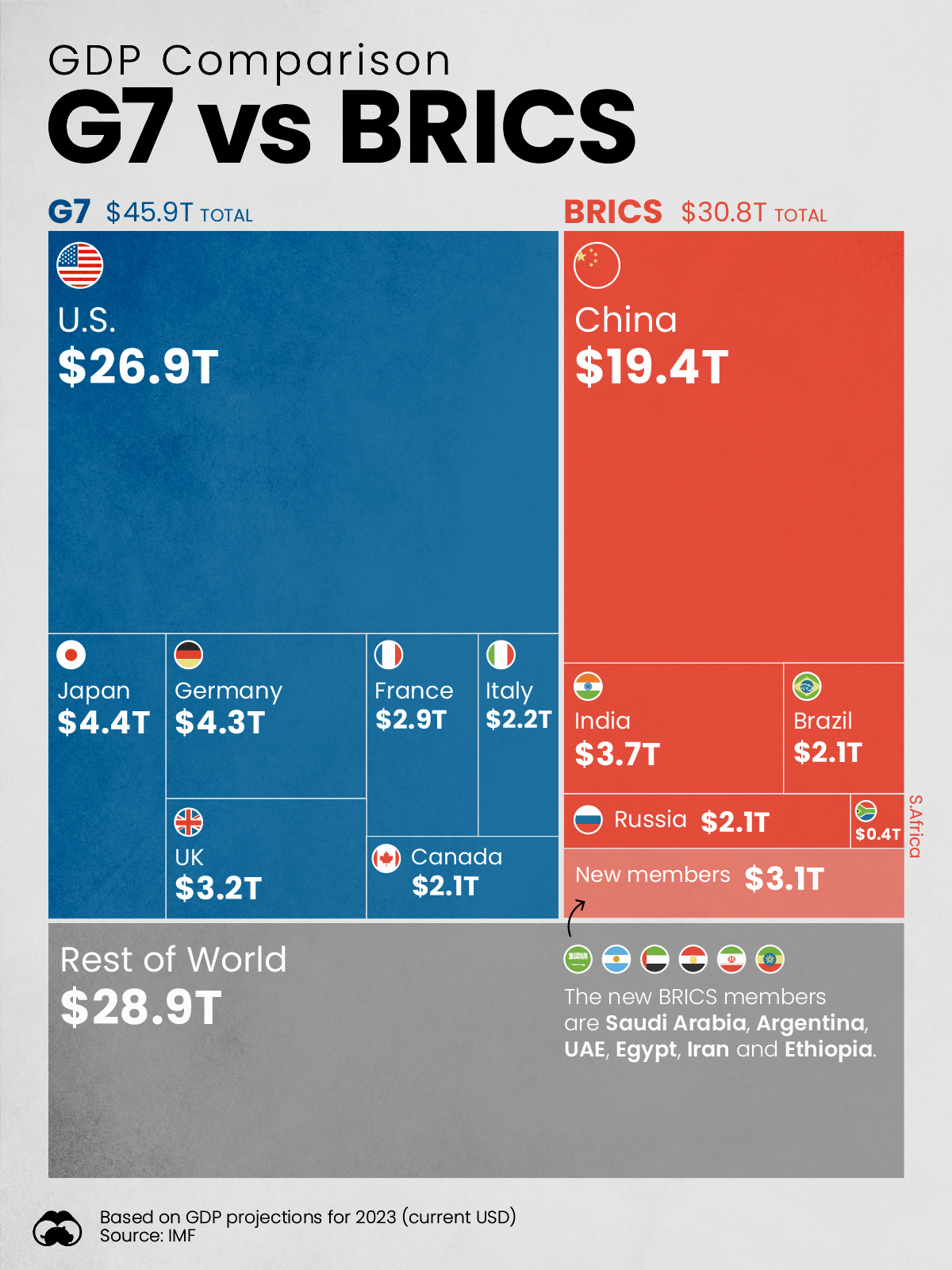

At Responsible Statecraft Michael Corbin remarks on the meeting of the BRICS+ nations (Brazil, Russia, India, China, South Africa and now Egypt, Ethiopia, Iran, and the UAE)—representing nearly 40% of global GDP and 45% of the world’s population:

Despite objections from some BRICS+ members, it seems as though de-dollarization is slowly moving towards an economic reality. According to the Jerusalem Post, China has already unveiled plans to use a gold-backed yuan and Russia is trading in currencies tied to gold. Together with the significant gold accumulation by BRICS countries, these actions suggest a world shifting away from dollar reliance. For example, the divergence between treasuries and gold as safe havens has signaled investors’ heightened uncertainty given skyrocketing government debt and their preference for physical assets. Over the last 10 years, central bank purchases of gold have significantly outpaced purchases of U.S. Treasuries.

The Kazan BRICS summit has demonstrated a considerably impressive level of ambition, no doubt fueled by Russia’s chairmanship and the many underlying financial and economic issues with which it is currently wrestling. Although Russian interests obviously are driving the current agenda, it is evident that the issues presented resonate strongly among a variety of countries, from global powers like China to nations throughout the Global South. They all share a common interest in navigating the emerging challenges presented by a rapidly developing multipolar architecture.

Although BRICS 2024 is unlikely to implement immediate solutions to its economic and finance proposals, it has already successfully generated enthusiasm for alternative approaches to the post-World War II order. After several decades of war and harmful sanctions, BRICS+ nations are increasingly distrustful of the United States led “rules-based order” that favors the few at the expense of many. Western nations should take notice that while BRICS will not immediately bring down the existing global architecture, it is a looming threat to the unrivaled dominance of its institutions, which no longer maintain the trust or confidence of a growing majority of the world’s inhabitants.

Shorter: we’ve screwed up. Not only have we screwed up but whether Harris or Trump is elected president we are likely to continue to screw up in just this way.

The consequences may be serious. For one thing if we are impelled to pay for our imports in something other than dollars it could cause a reduction in standards of living much more drastic than those being predicted for tariffs.

A possible end to the dollar as the global reserve asset would have beneficial aspects as well as negative ones.

Being forced to pay for imports with something besides dollars can also be phrased as imports would have to be balanced by exports (whether of goods or services); rectifying the trade deficit and all its ills. A world where gold was the reserve asset like means a much larger US industrial base than present. That’s why Luke Gromen often says we have a choice, we can choose to preserve the dominance of the dollar or we can choose to have a healthy manufacturing base.

The key to it all is the speed at which such a transition occurs. Can it be spaced out over decades rather than in a financial panic.

I am ambivalent on the US “screwing up”, I don’t think the US has made the best choices; but the countries in the BRICs (and practically everyone that is not a US treaty ally, or most of the world) have an evergreen incentive to diversify their exposure risk on US treasuries.

I will keep this as short as possible. Companies trade using an agreed upon currency. The buyer must have or be able to obtain this currency, and the seller must be able to offload or invest this currency.

Therefore, liquidity and investment opportunity are required for a currency to be used for trading. Most of the “dollars” are actually eurodollars, and they exist on off-shore balance sheets and bond markets.

An illiquid currency will command a higher premium to acquire for the trade, and with fewer investment opportunities, there will be a smaller or no return on it.

There is a lot more, but I do not feel like writing a dissertation. The US can and is eroding the attraction of dollar based financial assets and, therefore, eurodollar based financial assets. This will eventually result in reduced liquidity, but it will take a decade or two, at least.