Barry Ritholtz chimes in on whether businesses are holding on to more of their cash with this observation:

The average cash-to-assets ratio for corporations more than doubled from 1980 to 2004. The increase was from 10.5% to 24% over that 24 year period. That was the findings of a 2006 study by professors Thomas W. Bates and Kathleen M. Kahle (University of Arizona) and René M. Stulz (Ohio State). When looking for an explanation, the professors found that the biggest was an increase in risk.

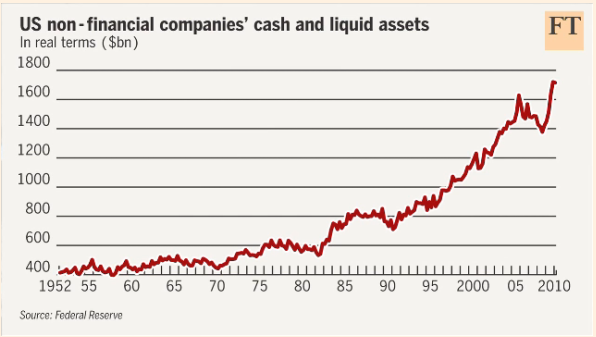

Indeed, the phenomena of corporate cash piling up has been going on for a long long time. You can date it back to the beginning of the great bull market in 1982 to 86, went sideways til the end of the 1990 recession. It has been straight up since then, peaking with the Real Estate market in 2006. The financial crisis caused a major drop in the amount of accumulated cash, but it has since resumed its upwards climb.

and includes this graph.

Well, yes. To my eye it looks as though between 1952 and 1986 the cash position of corporations has roughly doubled and then doubled again since about 1996. Since I’ve been complaining about this phenomenon since about that time and been doing it on this blog since this blog has existed it’s not surprising to me.

How does it refute the fact that businesses are holding on to more cash than they used to?

I’ve never complained that businesses were hoarding cash because Barack Obama was elected to the presidency. Check around. I’ve complained pretty routinely that businesses weren’t investing enough to promote future economic growth and hadn’t been for some time. In one of my earliest posts I pored over big pharmaceutical companies’ annual reports and other financial statements and arrived at the conclusion that R&D spending varied with inflation while marketing expenses (and, I suspect, the amount spent lobbying) varied with earnings.

The future is now.

{kind=link}

Barry swwwiinngss and…nothing.

Sorry Dave I find the chart to be so completely uncompelling.

Well, I guess not surprisingly, I find myself with Steve V here.

The graph is stupid on its face; the appropriate graph should be liquid assets as a percent of corporate assets, else we are just graphing the increase in total corporate assets, without acknowledging the sympathetic trend in liquid assets. That’s just dumb.

I’d have to do some homework, but if memory serves we will find that the ratio of liquid to total assets has moved from something like 5 to 6% over the past 40 years. We can debate the cause of this modest increase, but its hardly earth shattering. And I think it is hardly an indication of systemic deficient investment. That all said, there has been a recent spike in liquid assets. Why?

I have to admit that my world is smaller businesses, not large corporate. These stats that have been cited are really large corporate dominated, so there may be dynamics I’m unaware of. But I will tell you unequivocally (and at the risk of having the Mikey Reynolds of the world calling it “anecdotal”) that small businesses have pulled in their horns scared shitless at the current Congress and Administration’s posture. Just scared shitless. To be sure, there is a generic economic uncertainty, but the political environment has them frozen.

So this is look in the mirror time. Dave’s a serial entrepreneur, steve a small business medical manager…..and on it goes. What do you think? Example: You have a very good, and performing business. You cover the Midwest out of St. Louis. You have satellite ops for the NE, the SE and lower SW. But you don’t really cover the NW. Your business is growing nicely. Question: do we invest in a new warehouse/sales force/accounting function/ etc to access Seattle, Portland, Vancouver??

This is exactly the Board discussion held recently. Five years ago? Do it. Today? What are the costs of employment, the economic environment, the tax issues, the return? Thank you Nancy and Barry.

This is real, people, not just politics or some blog musings- jobs and capital deployment are truly at issue today. Wake up.

If Big Pharma had invested more in R&D earlier maybe the promise of pharmaceutical penis enlargement would be a reality by now. (With the side benefit of destroying the spam industry.)

Well, medicine is a service business, and an atypical one at that IMHO. It is privileged in many ways, but it is more susceptible to economic downturns than you might think. People dont want to take off for surgery when things are bad. More Medicaid hurts the bottom line.

I would be hesitant to expand anywhere unless I was pretty darn sure there were enough cases and the payor mx was good. That means I want solid businesses in the area. I dont really see any specific taxes coming up that will affect us as a business. Obamacare? I have come to dread every May when my insurance broker tells me that our insurer wants between 8% and 26% increases. Could it become worse? Maybe, but I am kind of inured to it. About 3 to 8 years out, I am worried about reorganization into ACOs or something similar.

I will note that this is the longest my nurses have gone w/o asking for a raise.

Steve

Michael swings and knocks one out of the park, humor wise at the very least. Thanks for the laugh Michael.

My beef with the graph is that it looks at absolutes and not the relative measure which is what we should be looking at.

This is a really confusing post. First, Ritholtz was responding to Fareed Zakaria, who was asserting that the accumulation of cash is a short-term trend. Matt Yglesias and others have been making that assertion as well, and as you note it’s just wrong. So he seems to be in agreement with you.

Second, the increase in cash has not been attended by an overall decrease in R&D – the Bates/Kahle paper that Ritholtz quotes is clear on this. They argue that R&D in the present day requires more liquid assets than in the past, but overall investment is up, not down. It may include a lot of bullshit investment, but that’s another story. Or perhaps there’s something wrong with their methodology – I’ll try to take a closer look at it another day.

There has been a substantial decrease over firm’s investments in fixed assets. Given that the conventional wisdom over the past 30 years has been outsource, right-size, small & agile this is not exactly surprising, nor is it clear to me that it’s a bad thing.