This post is a response to something in comments. These are all just round numbers. The aggregate personal income, that is, the total of all personal incomes in the United States was around $18 trillion in 2019. Roughly 150 million personal income tax returns are submitted annually. A little long division tells you that there are 1.5 million people in the top 1% of income earners. The gross collections from all personal income taxes is just under $2 trillion. The average income for someone in the top 1% of income earners is around $1.3 million per year—the median is much lower.

1.5 million X $1.3 million = $1.95 trillion. That’s the total income of all of the people in the top 1% of income earners. That means that the most you can realize in revenue just by taxing the top 1% of income earners is just under $2 trillion. And that would be by confiscating all of their income. Most of those people aren’t rich by anyone’s standards. Prosperous, yes, but not rich. Most are physicians, lawyers, and other professionals, middle level managers, and so on. It should be obvious that we can’t tax their incomes at 100%. They would be unable to pay their mortgages or feed their families.

According to the St. Louis Federal Reserve, the amount of federal taxes extracted from the economy as a proportion of GDP has varied from 5% (1930) to 20% (in 1945). It has never gone above 20% and for most of that period has been right around 17%. There is simply no political will in either political party to extract more.

Add up Social Security payments of various kinds, Medicare and Medicaid payments of various kinds, interest on the debt, and all of the other things the federal government spends money on and you come up with about $4.4 trillion. Total federal revenues in 2019 was about $3.3 trillion. We borrowed the difference. Under the CARES Act earlier this year we’ve spent something $1.75T and $2.25T more. We did that by borrowing, too.

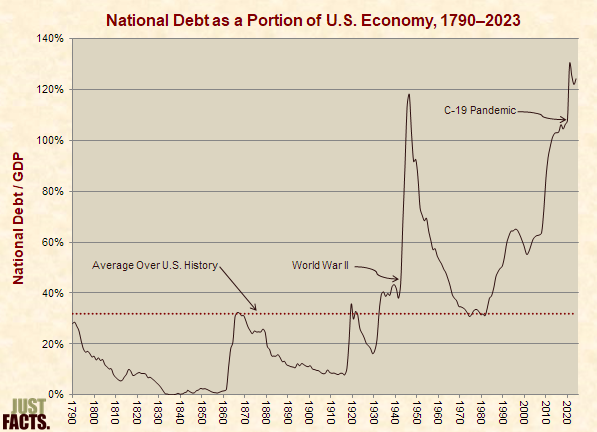

Let’s take a gander at the present size of that debt:

As you can see it’s the highest it’s been since 1945. We borrowed to finance World War II, too. There is strong empirical evidence that large public debt acts as a brake on economic growth. It used to be believed that there was a sort of cliff at 100% but that is no longer believed to be the case. Nonetheless the empirical evidence still supports the idea that public debt retards economic growth. Said another way after a certain level of debt it becomes extremely difficult to outgrow your debt. Do you see that dip in the graph in 1990 and the early Aughts? That’s what we did—we outgrew our debt.

There’s another alternative to borrowing, as those who support something called Modern Monetary Theory point out. We could just issue ourselves credit without actually borrowing the money, effectively inflating the money supply. I agree with them up to a point. I think that is safe and practical to do as long as you limit your expansion to the rate at which aggregate product is growing. Beyond that it will create inflation. I’m honestly not particularly worried about inflation at this point.

The bill that is presently being debated to extend supplementary income payments to those out of work would cost something between $1T and $3.4T (the HEROES Act). That would be in addition to the roughly $2T of the CARES Act.

The risk that concerns me is not inflation but hyperinflation. Hyperinflation is not just a species of inflation. It is a psychological and behavioral phenomenon—a catastrophic loss of confidence in the currency. Hyperinflation would be difficult for all of us but it would be disastrous for the very people the HEROES Act is trying to help. If countries like China and Japan which hold considerable dollar reserves decide the dollar is just too risky, it could provide a shock that spreads. It can happen very quickly and without a gradual period of high inflation as a warning.

Debt per se is not the problem. It can be, and is, rolled over. Interest is the killer. Even at our currently historically low interest rate, the annual interest payment will soon be the largest item in the federal budget. It squeezes out all other spending, especially defense and basic research. We might even be borrowing to pay the interest.

No one in Washington cares. No one on Wall Street cares. The voters don’t care. I got mine, Jack.

As I said the empirical evidence is that as the debt rises relative to GDP it retards growth.

But when you’re borrowing to pay the interest on the debt you have a different problem. It’s a positive feedback loop. The end is near.

Frightening thoughts.

Am I going to need a gun?

Modern Monetary Theory has effectively been adopted by both parties. COVID-19 caused Trump to abandon any pretense of caring about the national debt (not that he ever cared about it before) and the Republicans went along with it. IMO that’s one of the reasons for the push towards elimination of cash and forcing all transactions to be on-line, to track and then impose negative interest rates on savings to keep the jury-rig going until the current crew of thieves is out of office.

We may be headed for a repeat of what happened to the Ancien Regime. The debt the French monarchy incurred supporting the American colonial rebellion led to the French Revolution, Napoleon, and twenty-plus years of continent-wide bloodshed. My hope is we don’t come to that.

I guess I’m not seeing what we’re disagreeing about. I agree with basically all of what you’ve said. I agree that our present course is unsustainable, that there is a cliff and we very likely may not see that cliff until it is too late.

Is that reason enough to only spend the 1.1 Trillion we normally borrow for this year and no more for Covid? I get the sense that you are worried that spending for Covid will be the cliff or the catalyst that causes hyperinflation. That might indeed happen, but we don’t really know. The alternative of doing nothing is not exactly going to instill global confidence in the US or our future solvency.

My main point is that a crisis like this is the appropriate or at least a justifiable time to borrow and spend. If this spending will precipitate falling of the cliff it will be due to our collective decisions about spending over the last few decades, not due to any inherent problem with covid spending itself.

If we assume the amounts on the high end for the CARES and HEROES acts, then that’s about $5.5 trillion, or 5 years worth of our recent “normal” deficit spending. If $5.5 trillion is enough to put us over the edge, then we are already screwed as we would hit that 5.5 trillion in a few years. Probably much less than 5 since Covid is going to both reduce revenues and increase expenses resulting in more “normal” deficit spending in future annual budgets.

So in my view the problem isn’t spending on this or any other crisis event. A crisis, whether it’s a war, pandemic or something else, is when deficit spending is completely justified. The problem is our non-crisis status quo – borrowing to fund a substantial portion of the budget each and every year – a number that is continually growing with no end in sight. The inability to get that under control is, in my opinion, much more likely to result in a loss of confidence and hyperinflation than extra spending for a crisis that virtually everyone believes is necessary.

making holes in paper/metal targets is your idea of fun go for it. Otherwise, there is no shoot to warn or wound, only kill, if unwilling to face a murder charge or deal with the revenge cycle, leave it on the shelf. Warm clothes from a thrift store and sturdy boots would be a wiser investment.

Will probably echo Andy a bit but borrowing now isn’t the problem per se. This is the time to do it. Rather it is the constant running up of debt when we are not in a crisis. The wonderful “Trump economy was just more debt driven growth. When the economy is performing well we need to pay off our debt.

“Warm clothes from a thrift store and sturdy boots would be a wiser investment.”

There is a whole genre of apocalyptic fiction. Some of it isnt bad and as a hard core sci fi fan I have read some. Those authors seem to think that tools, cooking implements, seeds, means to preserve food, spices, salt and pepper, dried foods, rope, solar panels and lots of other things will also come in handy.

Steve

There is a great difference between borrowing when debt is 60% of GDP and when debt is 120% of GDP. If it can be done without blowing the entire system up, as you say, it would be justified under the circumstances but it should certainly be done with more prudence than either the CARES Act or the HEROES Act. If it can’t it will be disastrous.

Seriously if you believe that this could happen Silver Eagles are a low denomination bullion.

You’ll pay a premium to buy but they should hold their value in a crisis.

But anyone who holds precious metals in their home will need tight lips, people talk and the world is a dangerous place.

I don’t know how worried to be but I think the very least that those who want to incur substantial debts should be doing is proposing a mitigation plan along with their spending plans.

“There is a great difference between borrowing when debt is 60% of GDP and when debt is 120% of GDP.”

Definitely. Without CARES or HEROES we’d still be borrowing well over a trillion this year and that is only going to go up. We are incurring substantial additional debt every single year. That’s the structural problem that needs to be addressed.

Andy and steve’s logic is horribly off base. You can always argue that the current particular and “needed” spending program is warranted. Why of course it is. That’s how you eventually become a bug on a windshield, which is what Dave is really getting at. The correct argument is how you ration between spending A, vs spending B. Else you believe in fairies, or you are a politician. It is called economics, you know.

To pour gas on the fire. Some of us have greater financial capacity than others, and maneuvering room in asset allocation and upside. As you cavalierly dismiss what’s going on, or offer petty political observations, remember that if the shit hits the fan, you will be disproportionately harmed. And because of the levers you have pulled, it will be a self-inflicted wound. I hope you think it was worth it.

“The correct argument is how you ration between spending A, vs spending B.”

We pretty much just did. Spending to help make Trump look good was bad and drove up our debt. Several of us here argued against it. As I recall you were either mute or supportive. We need to find ways to grow without deficit spending. Spending when UE is at 20% is, some of us believe, a better case.

@Dave Schuler

…. If countries like China and Japan which hold considerable dollar reserves decide the dollar is just too risky, it could provide a shock that spreads. …

You were not doing bad up until this point. It is theoretically possible but highly unlikely to occur.

China’s internal banking system leverages dollars to create renminbis. The yuan is used to swap for dollars in foreign trade. Japan and the rest of the world use the dollar for global trade because dollars are more available for currency swaps.

The Modern Monetary System is a financially based system, and currency is created through lending. Mortgages are created by the private sector bank “printing money”.

Since that private sector “printed money” is ultimately government backed, the “market based free enterprise system” is nothing more than a lot of self-righteous assholes whining about people getting “free-stuff” while becoming rich because of “free-stuff”.

After LBJ removed the gold cover in 1968, base money ceased to exist. Currency creation was no longer limited by the gold supply. Instead, it is limited by assets, and anything that can be collateralized can be an asset used to create currency.

Bretton Woods allowed dollars to be exchanged for gold, and Nixon was forced to default on the dollar to keep the US gold supply from being depleted. There ceased to be a “reserve currency”, but because of the well established eurodollar system, dollars continued to be used for global trade.

The standard fractional reserve lending example assumes base money. In the MMS, the $100 that Joe deposits in Bank A was created when Judy deposited $110 in Bank Z, Sam borrowed $100, and he paid Joe $100 for a car repair.

Money creates loans, and loans create money. Conversely, repaying loans destroys money. Repaying the $20T US national debt would destroy $20T. I doubt that would help the economy, but what do I know?

MMT is based upon the MMS and its implications, but in my opinion, it fails to fully understand the financial system, global trade, and their implications.

Income & wealth inequality are a direct result of the MMS. Those who lend make money and obtain wealth, and more lending creates more money and more wealth for the lenders. Not so much for the borrowers, but being an MMTer means never having to say your sorry.

Increasing taxes on those lending results in increased lending to pay the increased taxes and increased income & wealth for those being taxed. When the wealthiest people are screaming to be taxed more, it should be an indication that there is a scam somewhere. Honestly, you do not get that rich without a scam.

Because fewer currency swaps mean fewer dollars are needed, weakened global trade would lead to weakened dollar, but hyperinflation is highly unlikely. Furthermore, the US owns enough collateralizable assets to increase the national debt by an order of magnitude or more.

petroleum reserve – collateralizable

national park revenue – collateralizable

Library of Congress – collateralizable

Lincoln Memorial – collateralizable (mortgage)

etc.

BONUS FACT – Destroying statues destroys MMT money.

The wisdom of “mortgaging everything to the hilt” is another matter, but extending uncollateralized backed credit in the MMS is nonsense. It is akin to dividing by zero, but if you do not understand what that means, you probably think MMT allows unlimited credit creation.

Unrelated Side Note:

The Commerce Clause of the US Constitution allows Congress to create and the Executive branch to enforce regulations affecting interstate commerce. Wickard v. Filburn established that everything affects interstate commerce.

If a customer’s stinky fart could cause another customer to leave before purchasing desert, the stinkiness of the fart can be regulated, and therefore, any of the causes of the stinkiness of said fart can be regulated.

When President Trump says that he has power to do something, he probably has the power to do everything.

@Drew

… It is called economics, you know.

Actually, what is called economic is like Newtonian or Medieval physics. The Modern Monetary System is like Einsteinian physics. Energy and matter can be converted to each other – so too with money and credit. You can work out the quantum mechanics and dark energy aspects.

Burn, Baby Burn

‘There is a whole genre of apocalyptic fiction. Some of it isnt bad and as a hard core sci fi fan I have read some. Those authors seem to think that tools, cooking implements, seeds, means to preserve food, spices, salt and pepper, dried foods, rope, solar panels and lots of other things will also come in handy.’

The first thing a survivalist should do is figure out who is hoarding survival supplies, where, and how strongly is that hoard defended. Why go to all the trouble and time and expense to hoard when you can steal someone else’s? Of course that means buying guns and ammo first (and perhaps equipping yourself with sniper scopes and night sights) and training with them until you’re a good shot. But then you’d still need that stuff to defend what you took.

Me, I’d rather try to hold things together. I’ve read enough history, including about the joys of living during the Warring States period in China or during the end of the Western Roman Empire, to not want to live in a repeat of those times.

I stopped reading SF about 20-30 years ago (kept buying the occasional Fantasy novel until recently) when it started getting to preachy and feminized for me. Any particular authors you like?

Al of the old classic authors Iliekd and read. Lucifer’s Hammer is maybe the classic post-apocalyptic sci fi book, though you might might count Time Machine by Wells. Of late i have liked Pierece Brown, Brin, Bear, Liu Cixin (maybe the best of the new Chinese writers) Jemisin, Wells” Murderbot series, Bennett, Leckie, some Anders and a bunch of others.

Steve

i haven’t mentioned it lately but I’m a collector of 19th and 20th century science fiction, fantasy, and horror. I’ve posted about post-apocalyptic science fiction several times over the years, most recently here. One of the earlier efforts, M. P. Shiel’s The Purple Cloud, includes many of the themes that have become familiar.

Good to hear from you, Tasty. I miss you, seriously.