There’s a post over at Outside the Beltway I’d like to draw your attention to on the decline of war from the second half of the 20th century to the present. I’d intended to comment on this in a post of my own but his will do. Here’s a snippet:

In a mass media environment where we hear about horrible events from all over the world every day, it’s easy to think the world is falling apart. Or at least getting worse. But, according to Harvard Prof. Steven Pinker, the world has been becoming more peaceful and less violent throughout the history of civilization–and continues to do so&@133;

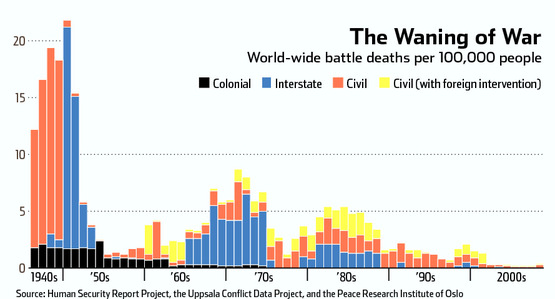

Take particular note of the graphic attached to the post. I won’t bother reproducing it here but, since much of this post is based directly on it, the post may not make a great deal of sense to you without it (it may not make much sense to you with it but that’s another issue).

First, if you needed a graphic illustration, literally, of the Pax Americana, the American Peace, for good or ill here it is. All of the spending (and borrowing) borne by Americans, all of the loss of life has bought this. We have made war futile. Attention must be paid.

That would probably be denied vehemently by some (which is largely why I’m posting this here rather than at OTB) and I recognize that the Europeans, in particular, reject this explanation. IMO it’s blindingly obvious and has some implications. Our challenge going forward is to preserve the peace while doing it at a cost we can bear. I sincerely believe that in a couple of centuries the history of our times will be seen by how successful we are at that.

Second, look at the jump ups in the light blue bars, the increases in battle deaths in interstate war. With two exceptions those jumps are when America went to war, first during the Second World War in the 40s, Korea in the 50s, Viet Nam in 60s and 70s, and the first Gulf War in the 90s. The jump during the 1980s is almost certainly primarily due to the war between Iran and Iraq while the jump in the late 1990s was presumably due to a number of small, bloody conflicts that took place largely without the notice of the American media because we weren’t involved in the fighting.

The wars in Iraq and Afghanistan are invisible. Painful and costly as they’ve been to us they haven’t provided the number of battlefield deaths that previous wars have done.

Finally, how you choose your terms is important. The graph reflects battlefield deaths in interstate wars, civil wars, and colonial wars. It does not reflect the hundreds of million of deaths due to countries killing their own people. We will never know how many people were killed in Germany, Russia, Eastern Europe, China, Cambodia, Iraq, Iran, and so on, murdered by their own governments. They don’t show up on the chart.

Were these deaths added to the chart it would strip away any illusion that the present is less violent than the past. But Leviathan’s hand reaches only so far.

{kind=link}