This column from the Detroit Free Press may cast a little light on the point I made yesterday, that healthcare costs, specifically in the form of healthcare insurance premiums, are rising sharply although incomes are declining:

In the past few days, 114,000 Michigan households have received bad-news letters from Blue Cross Blue Shield of Michigan, socking individual health insurance subscribers with premium increases averaging 22%, effective Oct. 1.

Blue Cross could have said, “Hey, things could have been worse. We asked for a 56% rate hike first and dialed it back to 22%” — but that probably would have just made folks angrier.

Instead, the Blue Cross letters simply stated, “We know every Michigan resident faces financial challenges, and we thank you for your business and loyalty to the Blues.”

Insurance is highly regulated, mostly by state governments (typically in the form of insurance regulation boards). In Michigan state law requires Blue Cross to insure all comers and it also requires that the company not lose money on its insurance products:

State law requires Blue Cross to offer insurance to anyone, but it also demands that the company not lose money on its insurance products. Therein lies the rub: Blue Cross lost $133 million last year on individual subscribers.

It isn’t just individual premiums that have risen in Michigan. HMO’s have increased their rates:

“Increased efficiencies by Michigan HMOs allowed them to improve their income last year — up to a slender 2.6 percent of premiums — despite low premium increases and declining enrollment,†said Rick Murdock, executive director of the Michigan Association of Health Plans.

But premiums may be going up more this year to more closely match rising costs, according to interviews with HMO executives and OFIR data.

Hawkins said Priority has increased premiums an average of about 6 percent, although the effective premium increase was lower because some companies changed benefit plans that cut costs.

Kluge said Blue Care increased premiums 7 percent to 8 percent.

Additionally, Blue Cross won approval from state regulators for an average 4.7 percent interim increase on its supplemental Medicare policies, known as Medigap, which are held by about 210,000 seniors.

Insurance commissioner Ken Ross ruled that Blue Cross had proved it needs the interim increase to stave off losses.

Blue Cross, however, will continue to seek its original request of an average 31 percent rate hike on three Medigap plan options. The insurance commission is expected to make a final decision on Nov. 6.

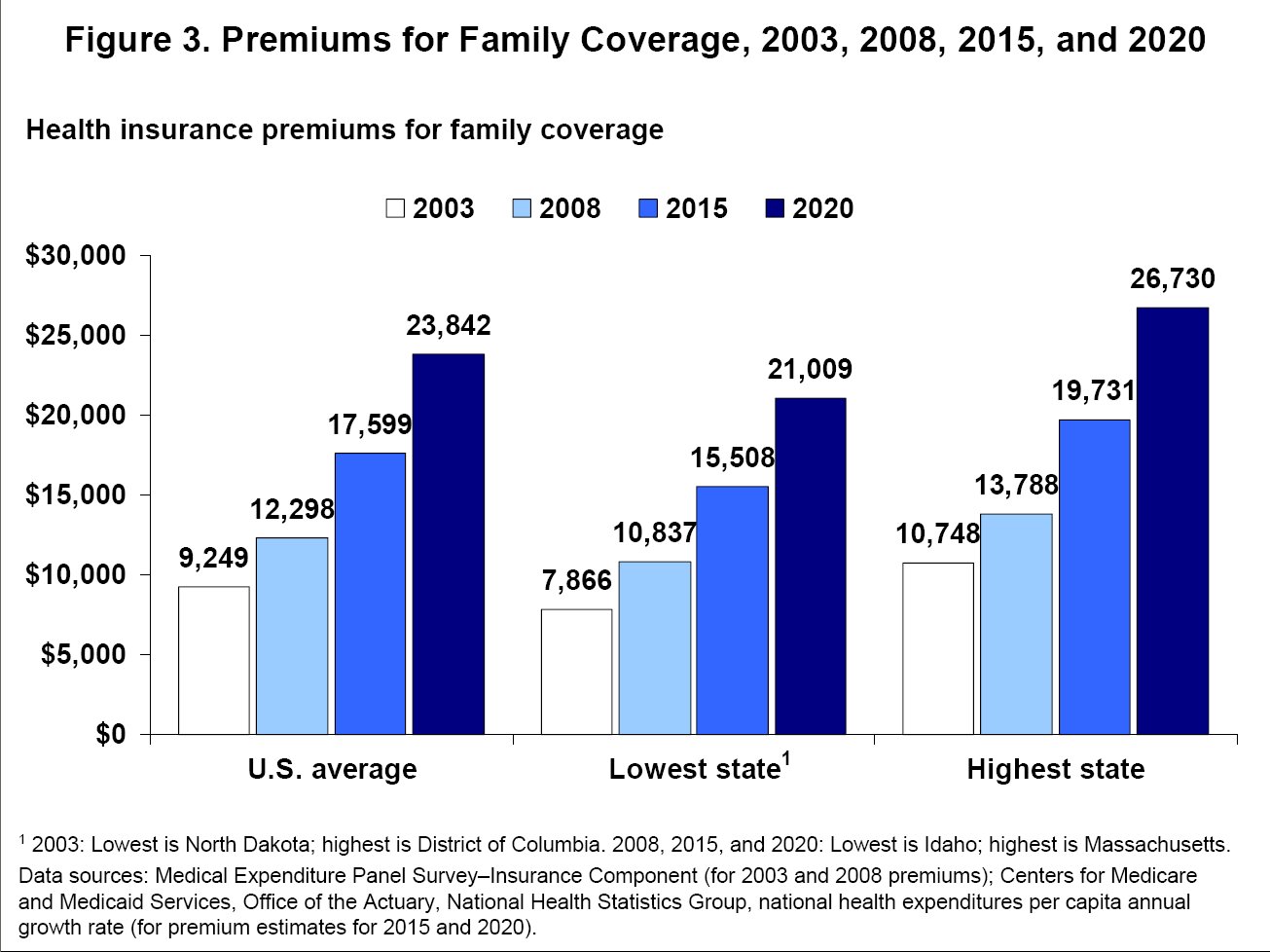

Nationwide premiums for family coverage in employer-sponsored have increased 119% over the last decade:

Family premiums for employer-sponsored health insurance in the U.S. increased 119% between 1999 and 2008, far, far higher than any increase in wages, according to a new survey. If current trends continue, premiums are on course to increase another 94% by 2020, to an average of $23,842 per family. Employees pay on average about 30% of this amount.

The study, by the non-profit, non-partisan Commonwealth Fund, found that in 2008 total premiums—the amount paid by both the employee and employer—equaled or exceeded 18% of the average household income for the under-65 population in 18 states, compared to just three states in 2003. In Mississippi, Tennessee and West Virginia, family premiums averaged 20% or more. Southern and South-central states in general felt the pain of rising premiums the most, because incomes are lower than national averages.

There are some great charts and maps of the premium increases on a state-by-state basis here. One of the charts is pictured above. They provide a virtual definition of unsustainability. I don’t just mean unsustainable for individuals and companies. I mean unsustainable for the federal government, too.

The insurance companies attribute the increased cost to increased pharmaceutical cost, higher utilization, and increased provider costs.

When I did my research on this while writing a proposal (modest and limited to specific issues) for our Congressman, the insurance people I spoke with claimed that much of the increase was also due to losses on investments. For my small corporation they wanted a 26% increase (Pennsylvania) this year. Private insurance has been worse at holding down costs than government insurance. This will be even worse with this recession.

On the larger issue, this is what makes health care costs so hard to control (one of several issues). Given our tech and the desire to have first world quality medicine, I do not see we can function without some form of insurance. Under almost any system, the costs of major illnesses are too high to cover without insurance. Yet, once you add insurance to the payor mix, it is too easy to mine. There is too much information asymmetry. The decisions on major spending are made by people under stress, not detached perfectly rational bloggers. The decisions are often made by the elderly who have trouble understanding all of this tech.

Steve

There are two ways to make money in the insurance business: investments and the insurance business. However, the situation in Michigan is distinctive: state law requires that insurance plans at least break even on their insurance business. That’s why Michigan is such a great example. You can disaggregate the investment part from the insurance part.

It might just be me, but the difference btw/ the staes in the state-by-state chart, appears modest. Except perhaps Massachusetts, it would appear to my eye that state policies (mandatory coverages) probably have relatively minor impacts on costs. Instead, high cost-of-living areas have higher costs. Areas with less access to healthcare, such as the Northern Plains have less costs. Places with unique demographic populations, like Hawaii, reflect their uniqueness.

I think you’ve read the code on Hawaii, PD. High proportional rate of first generation East Asian immigrants. I suspect there are other cultural and genetic reasons, too.

Nice post Dave, as usual well presented, with appropriate links. When President Obama states that current system is unsustainable, to me it seems strange that various pundits just simply do not explore that statement. Maybe ideology creates a tunnel between the ears, to old in one ear, and out the other.

This argues for the importance of the “public optionâ€:

Said it before, but I will say it again, there is just too much money to be made in this game. Care to hazard a guess what the top echelons of the Blues in Michigan make, and whether they received a salary increase over the past year? Meanwhile, we have this, and if Insurance Companies are to make a profit, their shrinking client base mandates an in crease in fees to their remaining customers.

Any “reform†without a public option is delusional…

R. Paul Miller, MD

I think the current system is unsustainable with or without the public option unless other reforms are included as well. I don’t have a problem with a public option or even with single-payer if other reforms are also adopted, particularly those intended at reducing demand and increasing supply.

Without those any reform will simply be a license to print money. As you put it “there is just too much money to be made in this game”.

I think Our Paul is demonstrating his idealogical blinders.

After invoking the red herring that insurance company execs make too much money, he then laments that public officials are giving insurance companies too good a deal…………and then suggesting that a public option – where all the good and wise public officials will reside I guess – is the solution.

Now THAT’s delusional.

Steve – I’d suggest that you observations about insurance are overwrought. People successfully insure for big bucks issues with cars (damage and liability) all the time. They do the same for homes, most people’s biggest financial asset. Health care insurance is not so unique.

If put into place early in life (beginning of working career) and if portable with no indiscrimint cancellation provisions, health care insurance is not so complex. And not an expenditure that must be dealt with under duress or by the confused.

Our Paul set up a straw man: nobody understands Obama’s assertion. What? Of course they do. Our blog proprietor has hammered it forever. In my daily life I observe that people understand. But certain elements of “reform” are rather easy to understand, and don’t come close to the draconian House proposal:

1. Make it catastrophy insurance, not a maintenance contract.

2. Make it portable. (Probably meaning divorce it from the employer.)

3. Create high risk pools.

4. Do something about the lobbying problems cited by OP. (Wait, that’s a pipe dream.)

Separate from insurance, I’v gravitated over to one of DS’ points – supply. But I’m still thinking its a second order effect in the absence of a demand throttling reform: price.

Drew-Sorry if I was unclear. I believe insurance distorts incentives. Yet, I see no way around it. When I was talking about the confused and stressed patients, I was talking about making specific treatment choices, rather than their choice of insurance. Btw, my list of priorities has costs first, portability second then expansion. I dont think costs is politically feasible now, so hope for some of the other reforms.

I am also skeptical, to some degree about supply. It is nice theory, but when you look at places like cities with lots of medical care, it usually costs more. The physician, heck even the PA who would replace them if that is your goal, is often just a force multiplier. It is the tests and studies and treatments ordered that will drive costs. The tests and medications I just ordered in the ICU will cost way more than what I make for several days, and it is a slow day here. Those tests and meds would cost the same if ordered by a PA, a nurse or a janitor. Also, practical experience with extenders shows me (we actually use them a lot already) that you can save some, just not as much as it would first appear. You need to plan for time off, lunches, breaks, overtime, etc. that you do not have to do with docs.

Finally, how do you get from here to there? Let us say we announce we are going to greatly increase the number of docs in order to cut down salaries and save money. Who signs up?

Dave-Thanks for the clarification on Michigan as I misread. Mea culpa.

Steve

Drew, my good man, I do not think it is an ideological difference that we are dealing with, but a perception difference. Our current health care system is unsustainable as pointed out by the graph Dave Schuler presented. The projected outcome is shrinking availability of health care, an ever increasing pool of sick people, with resultant unsustainable debt that will drain our economy when they become ill, or enter the Medicaid or Medicare system.

There is no counter weight you presented to the Insurance companies, other than enforced regulation. The enforced regulation you suggest:

Is a bit of over simplification that leads one to wonder, in Barney Franks great words, what planet you are living on.

The problem is not only “indiscriminate cancellations†but the ability to purchase insurance with pre-existing conditions, which strangely enough may include the fact that you are of child bearing age.

I would go a bit further than examining a perception difference. We probably fundamentally disagree on the function of government. In my view, government’s function is to ensure to common good, not to ensure unrestrained free markets. We found out what happens when banks are poorly regulated under rubric of the magic of the market place. My comments about remuneration to the top echelons of the Blues in Michigan was a gentle reminder of the mess the banking and credit card industry created.

Insurance companies main function is making money, not health care. Once that is understood, the public option, as a counter weight, is inescapable.

If put into place early in life (beginning of working career) and if portable with no indiscrimint cancellation provisions, health care insurance is not so complex.

Is a bit of over simplification that leads one to wonder, in Barney Franks great words, what planet you are living on.

Actually I don’t see the problem. This solves the problem of pre-existing conditions for many cases. Suppose you take up insurance at time t, then at time t+s you develop a problem. If it is a persistent problem then you’d have a pre-existing condition if you try to swith insurers. But with Drew’s suggestion would solve that problem. Instead you’d have an option for renewal with no rate increase such an insurance contract could be developed. It would likely be higher in those periods when you don’t have this persistent condition, but it you can’t have something for free.

Why is this strange? Women of child bearing age don’t usually get unexpectedly pregnant. A woman isn’t walking down the street when SURPRISE she’s pregnant. In many cases it is something people actively work towards. Would you be surprised if an auto insurance company wasn’t thrilled with the idea of insuring people who actively work towards getting into an accident?

What is common good and how do we go about making sure its provided in just the correct amounts. Medicare ain’t it in case you are wondering because its a system that is horrifically out of whack and one reason we are in the mess we are in. Voting is horrible mechanism for allocating resources. You really want it to be a popularity contest on what kind of medical care you get?

And you’ve also offered a strawman argument here. It clearly isn’t a debate of common good vs. “unrestrained markets”. Nobody, but nobody is making the latter argument. To pretend otherwise suggests you are being deliberately misleading and dishonest.

And lets ignore the issues with rent seeking by large corporations with lobbyists sitting in nice comfy offices in K-Street.

Our banking system is not an unregulated market. In fact, two of the people that worked in that market are now sitting making big time decisions in Washington D.C. You don’t think that might be part of the problem. Oh, make it three if we count Mr. Emmanuel who sat on the board of Freddie.

This is true of all corporations. This logic would lead to a public option for cars…oh wait Government Motors. Dang. Well, there’d be housing…oh wait Freddie and Fannie whome we are bailing out to the toon of tens of billions. Dammit! Bread! Yes a public option for bread…oh drat all those ag subsidies. Sugar! There we go, no…wait, protective tariffs on sugar making it more expensive than it has to be. Yeah, a public option, yeah that isn’t going to go horribly wrong. I mean large corporations never engage in rent seeking…or maybe I’m wrong.

Yes, I’m sure there is a pony around here somewhere.

Dang the double quoting didn’t work. The first 3 paragraphs were by Our Paul, Drew, then Our Paul.

Steve, got to give you a tip. The secrete of this game is to look at the “core†argument. Once that is fully understood, you try to find some low hanging fruit in what ever points I am making to burrow towards the “core†argument and try to invalidate that… A few minutes reading Paul Graham’s essay on How to Disagree will prove invaluable in formulating counter arguments, and choosing wisely in what points you should make.

While you are at Paul Graham’s site, I would recommend a quick read of his essay Writing, Brieflyâ€. If you had a firm grasp of these two essays you surely would not have wasted any time tickling your fun bone by writing the last paragraph of your comments. I do not know if there is a pony lurking in this thread, but your computer has been taken over by a very malignant drivel spirit.

The “core†of my position can be found in two different points. First, we have this:

Two colliding concepts, common good, and unrestrained markets. Perhaps in the future, when our views collide, you can keep these two concepts on mind. The second “core†position can be found here:

I think here we both agree. The question is how they are making money, and is it injurious to the “common goodâ€.

I am back from the fringes of the North Country of NY State, back to Rochester, where the web is at my finger tips. I look forward to our next encounter, and hope to explore how automobile insurance is really not the model you should use as the shinning light of the Insurance Industry…

Pssst 1#: Sad to say, Paul Graham provided no guidance on whether the malignant spirit that has taken over your computer is of the drivel, or dribble variety. At first glance, dribble should be the appropriate choice. Not wishing to make you wonder what Bob Cousy is doing in your computer, I chose drivel.

Sigh, just goes to show you we share the common gremlin. Failure to anchor the link properly.